Does a Fleet Fuel Card Pay Off? The Honest Breakdown for Small Fleet Owners

Here’s a number that should stop you mid-scroll: according to Motive’s Physical Economy Outlook 2024, 14% of total fleet payments at the small fleet level disappear to fraud or theft. If...

Here’s a number that should stop you mid-scroll: according to Motive’s Physical Economy Outlook 2024, 14% of total fleet payments at the small fleet level disappear to fraud or theft.

If your business spends $8,000 a month on fuel — not unusual for a 7-vehicle HVAC or plumbing operation — that’s over $1,100 walking out the door every single month before you’ve paid a single card fee.

The question isn’t whether fleet fuel cards save money. Most do. The real question is whether they save enough for your fleet size, on your routes, given what you’re currently spending on manual reconciliation and silent misuse.

What “Worth It” Really Means for a Fleet This Size

Fleet fuel card benefits for small businesses center on three things: per-driver spend visibility, fuel-only purchase controls, and per-gallon discounts or rebates. Whether any of those are “worth it” depends on whether their combined value — measured in dollars saved and hours recovered — consistently exceeds the card’s monthly fees plus any switching friction.

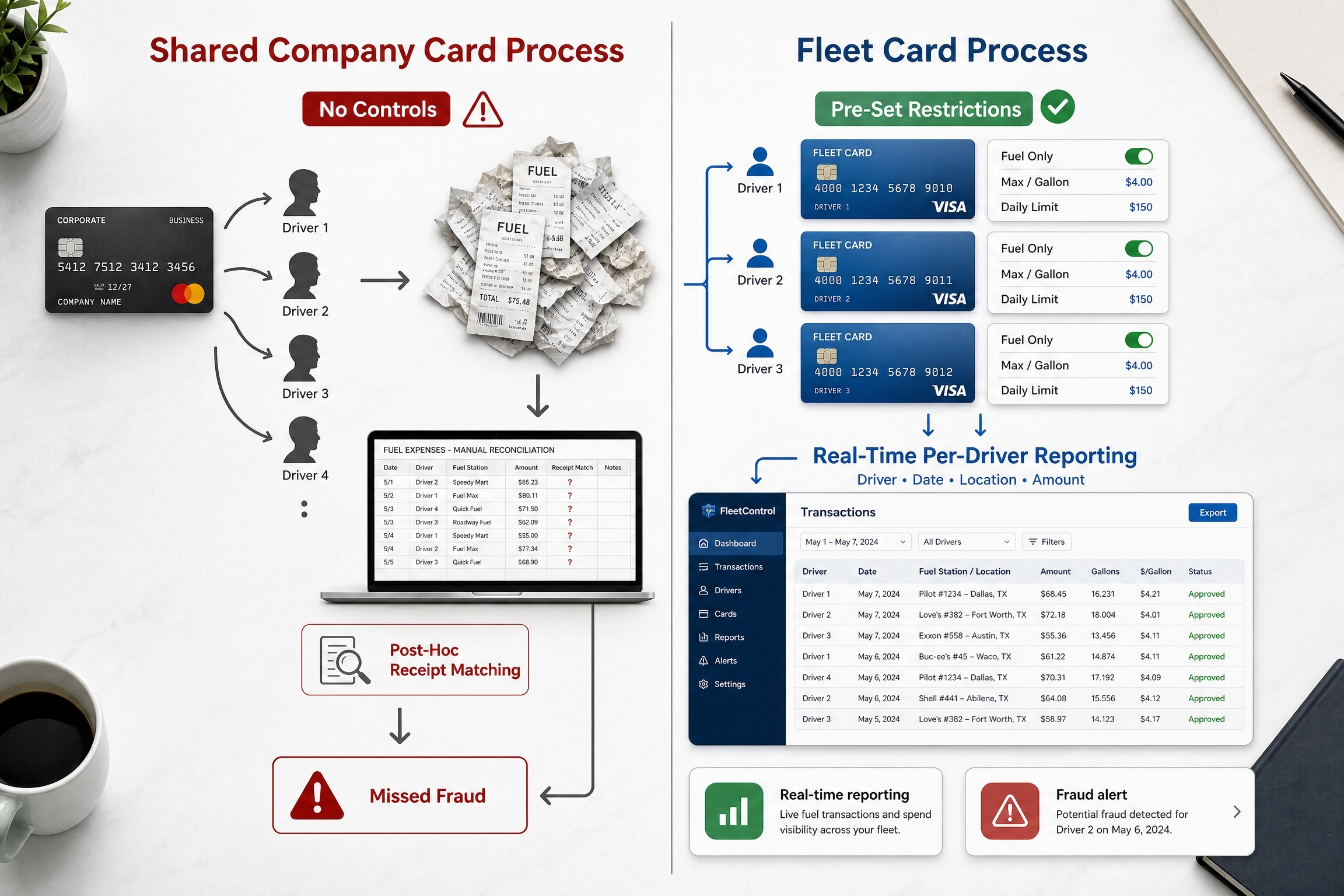

A fleet fuel card is a dedicated payment card that restricts purchases to fuel and fleet-related expenses, tracked per driver and vehicle. Unlike general business credit cards, these cards generate real-time spend reports, enforce pre-set purchase controls, and typically deliver per-gallon discounts through affiliated station networks. “Worth it” means the savings and recovered time exceed all fees and setup costs over a rolling 90-day window.

Whether fleet fuel cards are worth it for your small business comes down primarily to fleet size, monthly fuel volume, and how much time is currently lost to manual reconciliation. According to Motive’s Physical Economy Outlook 2024, small fleet operators lose an average of 14% of total fuel payments to fraud or theft — a figure that alone can justify the switch for operations spending $3,000 or more monthly on fuel.

The actual problem you’re solving

Small business owners who’ve managed fuel via a shared Visa often describe the same frustration: the card works everywhere, which is precisely the issue. No purchase category limits. No fuel-only enforcement. No per-driver accountability. Someone fills up on a Friday evening — work truck or personal car? You’ll find out six weeks later during month-end reconciliation.

Fleet cards solve the visibility problem first.

The per-gallon savings come second. What actually changes operationally is the accountability layer — restrictions are set before the swipe happens, not reconstructed after a statement arrives.

What most guides skip

Most fuel card comparisons bury the network coverage problem. The card with the best advertised rebate rate may deliver near-zero savings if your drivers’ regular fueling locations aren’t in-network. Mapping your drivers’ top fueling addresses against any card’s acceptance network should be Step 1 of any real evaluation — not a footnote.

The Break-Even Math — Where the ROI Actually Starts

The break-even point on a fleet fuel card for most small non-OTR operations sits at roughly 4–5 vehicles consuming 800–1,000 gallons per month combined. At a conservative 5¢/gallon discount on 1,000 monthly gallons, direct savings total $50/month — modest on its own, but fleet cards also eliminate the 3–4 hours of monthly receipt reconciliation that most operations managers absorb without ever naming it as a cost.

The fraud variable tends to tip the calculation decisively. For a business spending $8,000 monthly on fleet fuel, 14% exposure per Motive’s 2024 data represents $1,120 in monthly losses — losses that most purchase-control features on modern fleet cards eliminate entirely.

Running the calculation yourself

The following framework is a starting point, not financial advice. Consult your accountant for a cost-benefit analysis specific to your operation.

To calculate fleet fuel card ROI for your specific business, follow these steps:

- Pull your last 3 months of fuel spend. Calculate the monthly average.

- Multiply monthly fuel spend by 14% → your estimated fraud and theft exposure (Motive, 2024 benchmark).

- Multiply monthly gallons consumed by the card’s advertised per-gallon discount → estimated direct rebate value.

- Estimate hours currently spent on receipt reconciliation × your effective hourly rate → monthly time value recovered.

- Add all three figures. Subtract the card’s monthly per-vehicle fee (typically $0–$2/card/month for most major providers).

If the net figure is positive — and it nearly always is past 5 vehicles at standard service fleet volumes — you’re above break-even.

The number most owners miss

Some fleet management consultants argue that for operations under 5 vehicles, the administrative overhead of running a dedicated fleet card program outweighs the benefits. That’s valid when the owner personally reviews every transaction and no employee drivers are involved. But if you have even one employee driver with no purchase controls in place, the calculation changes significantly.

WEX’s own 2024 data shows customers with 21+ vehicles averaging $1,569 in annual rebates — roughly $74 per vehicle per year, or just over $6/vehicle/month. For a 7-vehicle fleet, that’s approximately $44/month from rebates alone. The real ROI driver for smaller fleets isn’t the rebate. It’s fraud elimination and the 40 hours per year recovered from manual reconciliation.

Fleet Fuel Card vs. Company Credit Card — What Actually Changes

Fleet fuel card vs. company credit card: A fleet card is better suited for fleets of 5+ vehicles because it provides per-driver spending controls, fuel-only purchase restrictions, and detailed odometer or mileage tracking. A business credit card works better for smaller operations with mixed vendor spend where universal acceptance matters more than purchase control. The key difference is where accountability is enforced — at the point of sale, not reconstructed from a monthly statement.

Quick Comparison

| Option | Best For | Key Benefit | Limitation |

|---|---|---|---|

| Fleet Fuel Card (WEX) | 5–15 vehicle service fleets | Per-driver controls, fraud prevention, rebates | Network restrictions at independent or rural stations |

| Company Credit Card | 1–4 vehicles, mixed vendor spend | Universal acceptance, flexible spend categories | No fuel-only enforcement, no per-driver visibility |

| AtoB Fleet Card | Diesel-heavy routes, 5+ vehicles | Up to 42¢/gal savings at partner truck stops (H2 2025) | Best savings only at in-network partner locations |

| Coast Visa Fleet Card | Mixed or EV-transitioning fleets | Universal Visa acceptance + EV charging network support | Less aggressive per-gallon rebate vs. network-specific cards |

Here’s the thing: most small fleet owners already know they’re losing money to misuse. The uncertainty isn’t whether losses are happening — it’s whether they’re $200/month or $1,000/month. Fleet cards answer that question definitively. And they prevent the losses going forward.

What actually shifts when you move from a shared Visa to a dedicated fleet card isn’t primarily the savings — it’s accountability timing. Drivers don’t recall what a $67 Circle K charge from three Fridays ago was for. They haven’t kept the receipt. The restriction happens before the transaction, not after a statement arrives.

When Fleet Fuel Cards Are NOT Worth It

This is the section most fleet card content skips entirely. Let’s be direct about it.

Most guides on this topic are written to sell cards. The goal here is to help you avoid signing up for one that won’t pay off for your specific operation.

The volume threshold that changes the math

Fleet fuel cards are probably not worth the administrative setup for these situations:

- Single-vehicle operations spending under $400/month on fuel where the owner personally reviews every transaction

- 2–3 vehicle fleets with under $600/month total fuel spend, where per-gallon savings won’t meaningfully exceed even a minimal monthly fee

- Operations where all drivers fuel at one predictable location and the receipt process is already under control at a 2-truck shop

The break-even threshold is real. A 2-vehicle landscaping operation spending $600/month total on fuel might save $7–$12/month in per-gallon discounts at best. Without active misuse or suspected fraud, that doesn’t justify the onboarding effort.

The network problem no one mentions

Look — if you’re running routes through rural corridors or specialized industrial areas, here’s what actually matters before you sign up: map your drivers’ top 10 fueling locations against the card’s acceptance network before committing to any provider.

AtoB’s strongest savings come at partner truck stops — well-suited for courier or light-trucking operations on interstate corridors. Less useful for residential HVAC technicians fueling at independent suburban stations where those headline per-gallon rates may not apply to a single stop on the route.

Coast’s universal Visa acceptance solves this specifically. The network flexibility trades off against raw per-gallon rebate rates — but if your routes don’t align with major freight corridors, network coverage matters more than the advertised discount figure.

Or maybe I should say it this way: the best fleet fuel card is the one your drivers can actually use without routing around it.

Three Cards Worth Comparing for Small Non-Trucking Fleets

Rates and network structures change. Verify current pricing directly with each provider before making a final decision. This is not financial advice.

WEX Fleet Card

WEX is the market incumbent. Built for enterprise scale, it holds up reasonably well for smaller fleets because of reporting depth and accounting software integration — it connects with most fleet management platforms and syncs with QuickBooks, which matters for lean back-office operations running on one admin.

Their 2024 published data shows customers with 21+ vehicles averaging $1,569 in annual rebates. For a 5–10 vehicle fleet, expect something more modest: roughly $300–$700/year depending on fuel volume and station mix. WEX’s platform strength is in controls and visibility, not headline rebate numbers.

Network discounts run strongest at WEX-affiliated stations. At independent or non-affiliated locations, effective per-gallon savings can lag the advertised rate noticeably. Know your station mix before assuming the headline applies universally.

AtoB Fleet Card

AtoB has moved aggressively into the small fleet space. Their advertised diesel savings reach up to 42¢/gallon at partner truck stops as of H2 2025 — genuinely strong for courier or regional delivery operations running diesel vehicles on predictable freight-corridor routes.

The caveat competitors won’t spell out: those savings apply at partner network locations that skew toward truck stops on major freight corridors. Residential-route-heavy fleets — plumbers, HVAC technicians, landscapers filling up at suburban gas stations — will likely see meaningfully lower effective savings than the headline suggests. Confirm your drivers’ top fueling addresses against AtoB’s network map before signing anything.

Coast Visa Fleet Card

Coast is the outlier in this tier. It runs on the Visa network, delivering universal acceptance — independent stations, branded chains, truck stops, and EV charging infrastructure. If you’re managing a hybrid fleet or planning a partial EV transition in the next 18–24 months, Coast is currently the only major fleet card incorporating EV charging network access.

I’ve seen conflicting data on Coast’s average per-gallon savings — some sources cite 2–4¢/gallon as a universal baseline, others cite higher figures for specific categories and locations. My read is that network flexibility and EV infrastructure readiness are the real differentiators here, not the rebate rate.

If raw per-gallon discount is the primary decision factor and your routes align with AtoB’s network, Coast likely isn’t the highest-ROI choice. But if route unpredictability or fleet electrification is on the horizon, it’s the strongest option in this comparison.

How to Make the Call in the Next 10 Minutes

To determine whether a fleet fuel card is worth it for your specific operation, follow these steps:

- Calculate your 3-month average monthly fuel spend and divide by your vehicle count.

- Multiply total monthly fuel spend by 14% — your estimated fraud and theft exposure (Motive, 2024).

- Map your drivers’ top 5 fueling addresses against network coverage for 2–3 candidate cards.

- Request a full fee schedule from each provider and calculate net savings minus fees.

- If net monthly savings exceed $50, start a 30-day trial on the card with the strongest network-route overlap.

Most providers offer a no-fee or low-minimum trial period. The real investment is 2–3 hours to configure driver profiles, set purchase controls, and pull the first report. That’s a one-time cost — against 40+ hours per year currently absorbed by receipt reconciliation.

One view some fleet owners push back on: fleet fuel cards are typically described as procurement tools, a way to secure better unit pricing on fuel. The case I’d make is that for most small fleets, fraud and misuse prevention is the primary ROI driver. The per-gallon discount is a bonus.

If you’re skeptical, run the fraud exposure calculation from Step 2 before reviewing any rebate figures. That number will do more to clarify the decision than any provider comparison chart.

Common Questions About Fleet Fuel Cards

What’s the best fleet fuel card for a small business with under 10 vehicles?

For non-trucking fleets under 10 vehicles, Coast offers the most flexible Visa-network acceptance including EV charging. AtoB delivers stronger per-gallon savings for diesel fleets on freight corridors. WEX is best if accounting software integration is the priority.

How do I calculate whether a fleet fuel card will save my business money?

Multiply monthly fuel spend by 14% for estimated fraud exposure (Motive 2024), add per-gallon savings × monthly gallons, then subtract the monthly card fee. A net result above $50/month means the card typically pays for itself within 60 days.

Should I use a fleet fuel card or a business credit card for my drivers?

Use a fleet fuel card for 5+ vehicles when per-driver controls, fuel-only restrictions, or odometer tracking matter. Stick with a business credit card for smaller operations where universal vendor flexibility outweighs purchase control granularity.

Why doesn’t my current company credit card stop drivers from misusing it for fuel?

Business credit cards have no category restrictions by default — they’re general-purpose tools. Fleet cards enforce fuel-only rules at the point of sale, requiring driver ID and odometer readings that flag misuse automatically before the transaction clears.

When should I NOT get a fleet fuel card?

Skip fleet fuel cards if you have fewer than 4 vehicles with under $600/month total fuel spend, you’re the sole driver reviewing every transaction, or your routes don’t pass any in-network stations for the card you’re considering.

No Comment! Be the first one.